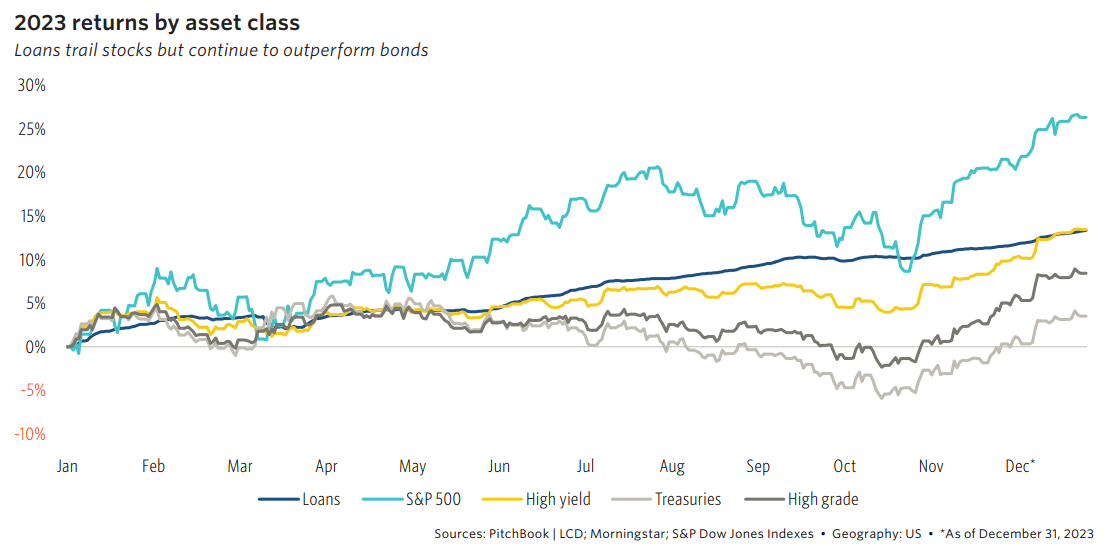

It was an exceptionally strong year for private debt funds, especially because of floating-rate corporate loans. In the US, leveraged loans gained 13.3%, and in Europe, they were almost the same at +13.4%. This was the best the US index has performed since the global financial crisis. Overall, private debt funds globally had an estimated return of 8.2% through the third quarter of 2023, which was the second-highest return among all asset classes in private markets.

Fundraising and dry powder in private debt

Private debt fundraising in the traditional institutional channel slowed down in the second half of the year. This was due to increased interest in more liquid alternatives offering similar returns. Around $76.7 billion was raised in private debt funds in H2, down from $112.6 billion in H1 2023. However, the total fundraising for 2023 is expected to surpass $200 billion for the fourth consecutive year. Private debt has now become the second-largest private market strategy in terms of annual fundraising, surpassing venture capital.

Private debt strategies

As the traditional fundraising slowed, private credit strategies saw a shift towards non-traditional sources, like loans, high yield bonds, and treasuries. These alternatives experienced returns ranging from -10% to 30% throughout the year. While loans trailed behind stocks, they continued to outperform bonds. Additionally, retail funds and separately managed accounts for insurers gained momentum in the second half of the year. Despite being outside our tracked universe, the seven largest publicly traded managers accounted for nearly half of all credit strategy fundraising, tapping into new investor markets effectively. Moreover, there was an unexpected surge in fundraising for BDCs that underwent IPOs.

Direct lending remained the top choice within private debt, making up 31.8% of total funds closed in 2023. Mezzanine and infrastructure debt saw significant increases proportionally. The product range within private debt is expanding, moving beyond its traditional focus on direct lending and distressed investments. Investment grade opportunities are emerging as a new area of interest. Asset-backed finance is becoming a focus for private credit managers, gaining ground from banks.

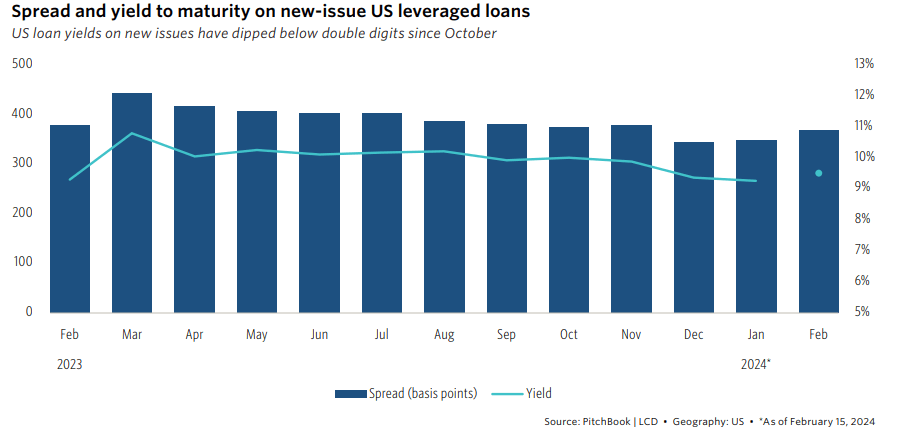

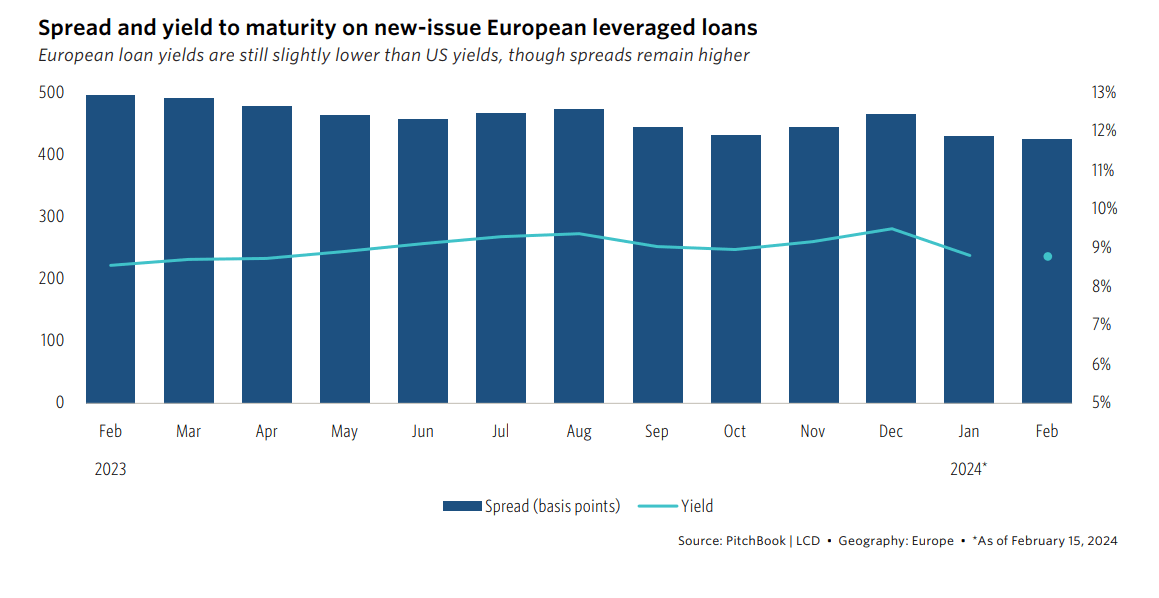

US and European market stats

While interest rates are higher today, investor appetite for private debt remains because in addition to the income generation, these funds provide diversification benefits, high risk-adjusted returns, and a hedge against inflation, among other benefits.’’

Jamal Hagler | Vice President of Research American Invest

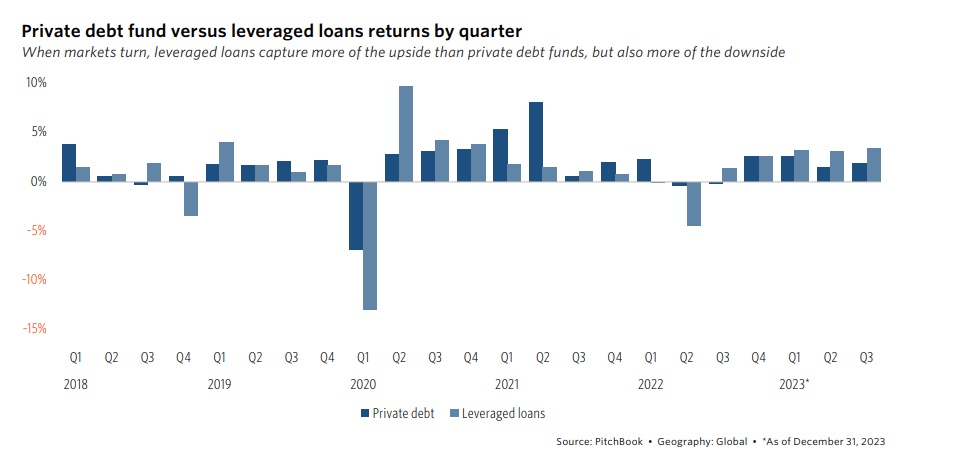

The consistently high yields are why private debt funds remain attractive and perform well compared to other strategies. Many are offering loans with yields equal to or higher than those in the bank-led syndicated market, which has slowed down except for refinancing and repricing. As a result, private debt is climbing up the performance ladder compared to other private capital strategies and currently ranks second highest, with a one-year return of 6.9% through Q2 2023. Our initial estimate for Q3 2023 suggests a trailing return of 1.9% over three months and 8.2% over 12 months, with less than half of our usual funds reporting so far.

Find your next investor-led CFO or Executive Finance role with Marks Sattin Executive Search

At Marks Sattin Executive Search, we work with a wide range of investor-led and privately-owned businesses across all sectors and locations. With over 30 years of experience, we have helped more than several professionals find their next exciting opportunity.